Navigating the financial landscape requires a clear understanding of both short-term and long-term goals. This exploration delves into the distinctions between these objectives, providing practical strategies and insights to help you effectively manage your finances. We’ll examine how to set SMART goals, implement effective budgeting techniques, and explore diverse investment options tailored to your time horizon and risk tolerance.

Ultimately, the aim is to equip you with the knowledge to create a comprehensive financial plan that seamlessly integrates both immediate and future aspirations.

Successfully balancing short-term needs with long-term ambitions is key to financial well-being. This involves careful planning, consistent saving and investing, and a willingness to adapt strategies as circumstances evolve. Understanding the interplay between these goals allows for informed decision-making, preventing short-term desires from undermining long-term prosperity. The following sections provide a roadmap for achieving this balance, fostering a secure and fulfilling financial future.

Defining Short-Term and Long-Term Financial Goals

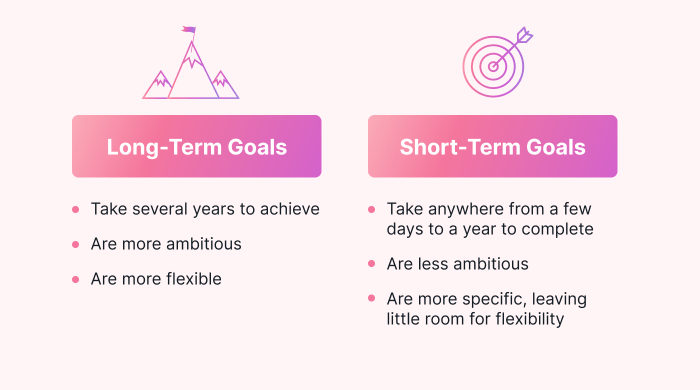

Understanding the difference between short-term and long-term financial goals is crucial for effective financial planning. Both are essential components of a robust financial strategy, but they require different approaches and timelines. Failing to distinguish between them can lead to missed opportunities and inefficient resource allocation.Short-term and long-term financial goals differ primarily in their time horizon and the strategies employed to achieve them.

Short-term goals are typically those you aim to accomplish within a year or less, while long-term goals extend beyond that timeframe, often spanning several years or even decades. The specific timeframe significantly influences the types of investments and financial products considered suitable for achieving each goal.

Timeframes for Short-Term and Long-Term Goals

Short-term financial goals generally have a time horizon of less than one year. These goals often involve immediate needs or desires. Long-term goals, on the other hand, typically extend from one to five years, or even beyond five years, sometimes spanning an entire lifetime. This longer timeframe allows for more complex strategies and potentially higher-risk investments with the potential for greater returns.

Examples of Short-Term and Long-Term Financial Goals

Short-term goals often focus on immediate needs and wants. Examples include paying off credit card debt, saving for a down payment on a car, or accumulating funds for a vacation. Long-term goals, conversely, focus on broader life objectives. These might include purchasing a home, funding a child’s education, or securing a comfortable retirement.

Comparison of Short-Term and Long-Term Financial Goals

| Goal Type | Time Horizon | Examples | Strategies |

|---|---|---|---|

| Short-Term | Less than 1 year | Emergency fund, paying off credit card debt, saving for a vacation, purchasing new appliances | High-yield savings accounts, money market accounts, short-term certificates of deposit (CDs) |

| Long-Term | 1-5 years or 5+ years | Buying a house, funding children’s education, retirement planning, investing in a business | Stocks, bonds, mutual funds, real estate investments, retirement accounts (401k, IRA) |

Setting SMART Financial Goals

Setting SMART financial goals is crucial for achieving both short-term and long-term financial objectives. A SMART goal is Specific, Measurable, Achievable, Relevant, and Time-bound. This framework provides clarity, direction, and a mechanism for tracking progress, ultimately increasing the likelihood of success. Without well-defined goals, financial planning becomes a vague exercise, leaving you susceptible to drifting without a clear destination.

Examples of SMART Short-Term Financial Goals

The following examples illustrate how to formulate SMART short-term financial goals. These are goals that can realistically be achieved within a year or less. Focusing on these smaller wins can build momentum and confidence, motivating you to tackle larger, long-term aspirations.

- Goal: Save $1,000 for a down payment on a used car. Specific: $1,000 for a down payment. Measurable: Track savings in a dedicated account. Achievable: Set aside $83.33 per month. Relevant: Supports the larger goal of car ownership.

Time-bound: Achieve this within 12 months.

- Goal: Pay off $500 credit card debt. Specific: $500 credit card balance. Measurable: Monitor balance reduction online. Achievable: Increase monthly payments by $

50. Relevant: Reduces debt and improves credit score.Time-bound: Pay off within 6 months.

- Goal: Increase emergency fund by $

500. Specific: $500 added to emergency fund. Measurable: Track balance in savings account. Achievable: Save $41.67 per month. Relevant: Enhances financial security.Time-bound: Achieve this within 1 year.

- Goal: Reduce monthly spending on entertainment by $

100. Specific: $100 reduction in entertainment spending. Measurable: Track monthly entertainment expenses. Achievable: Limit dining out, explore free activities. Relevant: Increases savings and reduces debt.Time-bound: Achieve this within 3 months.

- Goal: Save $200 for a vacation. Specific: $200 for a vacation fund. Measurable: Track savings in a separate account. Achievable: Save $50 per week. Relevant: Supports personal well-being and enjoyment.

Time-bound: Achieve this within 4 months.

Examples of SMART Long-Term Financial Goals

Long-term financial goals require a more strategic approach, often involving multiple steps and consistent effort. The examples below illustrate how to break down long-term goals into manageable, actionable steps.

- Goal: Buy a house in 5 years. Steps:

1. Save for a down payment (Specific amount, measurable progress tracked monthly).

2. Improve credit score (measurable through credit reports).3. Research mortgage options (specific lenders, compare interest rates).

4. Save for closing costs (specific amount, measurable progress tracked).

5.Find a real estate agent (specific agent, timeline for search). Relevant: Achieving homeownership. Time-bound: 5 years.

- Goal: Pay off student loan debt in 3 years. Steps:

1. Create a debt repayment plan (specific payment schedule, measurable progress tracked).

2. Explore debt consolidation options (research and compare options).3. Increase income (specific strategies, measurable progress tracked).

4. Reduce unnecessary expenses (specific areas, measurable reduction in spending).

5.Stay disciplined and consistent (regular tracking and adjustments to the plan). Relevant: Reducing financial burden. Time-bound: 3 years.

- Goal: Save $50,000 for retirement in 10 years. Steps:

1. Determine contribution amount (specific amount, measurable progress tracked).

2. Choose a retirement investment account (specific account, research different options).3. Invest consistently (regular contributions, measurable growth tracked).

4. Review and adjust investment strategy (periodic review, adjustments based on performance).

5.Consider additional savings strategies (side hustles, additional investments). Relevant: Securing financial future. Time-bound: 10 years.

- Goal: Fund a child’s college education in 18 years. Steps:

1. Determine estimated college costs (research, use college cost calculators).

2. Choose a savings plan (529 plan, other investment vehicles).3. Establish a regular savings schedule (specific contribution amounts, measurable progress tracked).

4. Monitor investment performance (regular reviews, adjustments as needed).

5.Explore scholarships and financial aid options (research, application process). Relevant: Supporting child’s education. Time-bound: 18 years.

- Goal: Start a business in 2 years. Steps:

1. Develop a business plan (specific plan with market analysis, financial projections).

2. Secure funding (specific funding sources, amounts, application process).3. Build a network (specific networking events, contacts).

4. Develop marketing strategy (specific marketing plan, measurable results).

5.Obtain necessary licenses and permits (specific requirements, application process). Relevant: Achieving entrepreneurial goals. Time-bound: 2 years.

Importance of Realistic and Attainable Goals

Setting realistic and attainable goals is paramount. Overly ambitious goals can lead to discouragement and ultimately failure. Consider your current financial situation, income, expenses, and risk tolerance when setting your goals. For example, aiming to save $100,000 in one year on a modest income is unrealistic, while saving $5,000 might be achievable. Similarly, investing heavily in high-risk ventures might be suitable for those with a high-risk tolerance and a longer time horizon, but unsuitable for those nearing retirement.

Adjusting goals based on unforeseen circumstances, such as job loss or unexpected expenses, is also crucial for maintaining motivation and achieving long-term financial success. Regular review and adjustment of goals ensures they remain relevant and achievable throughout your financial journey.

Strategies for Achieving Short-Term Goals

Achieving short-term financial goals requires a focused approach combining effective budgeting, disciplined saving, and strategic debt management. By implementing practical strategies, you can successfully navigate your finances and reach your objectives within the desired timeframe. This section will explore several key methods to help you achieve your short-term financial aspirations.

Budgeting for Short-Term Goals

Creating a realistic budget is the cornerstone of achieving any financial goal. A well-structured budget provides a clear picture of your income and expenses, allowing you to identify areas where you can save and allocate funds towards your short-term objectives. A step-by-step guide to crafting an effective budget is Artikeld below.

- Track your income and expenses: For at least one month, meticulously record all sources of income and every expense, no matter how small. Use a spreadsheet, budgeting app, or even a notebook. Categorize your expenses (e.g., housing, transportation, food, entertainment).

- Identify areas for reduction: Analyze your expense categories to pinpoint areas where you can cut back without significantly impacting your lifestyle. This might involve reducing dining out, canceling unused subscriptions, or finding cheaper alternatives for everyday purchases.

- Allocate funds to your short-term goal: Once you have a clear understanding of your income and expenses, allocate a specific amount each month towards your short-term goal. This amount should be realistic and achievable within your budget.

- Regularly review and adjust: Your budget is not set in stone. Regularly review your spending habits and make adjustments as needed. Life throws curveballs, so flexibility is key.

Effective Saving Methods for Short-Term Goals

Several methods can significantly boost your savings rate and accelerate progress towards your short-term goals. Consistent application of these strategies is crucial for success.

- Automate savings: Set up automatic transfers from your checking account to a savings account dedicated to your short-term goal. This ensures consistent contributions without requiring constant manual effort.

- Utilize high-yield savings accounts: Maximize your savings growth by choosing a high-yield savings account that offers a competitive interest rate. This can make a noticeable difference, especially over time.

- Round-up savings: Many banking apps offer a “round-up” feature, automatically transferring the change from your purchases to your savings account. While seemingly small, these increments accumulate quickly.

- Reduce debt: Paying down high-interest debt frees up funds that can be redirected towards your short-term savings goals. Prioritize debts with the highest interest rates first.

Debt Reduction Strategies for Short-Term Goals

High-interest debt can significantly hinder progress toward short-term financial goals. Strategic debt reduction is essential for freeing up funds and accelerating your savings efforts.

Effective debt reduction often involves prioritizing high-interest debts first, such as credit card debt. The snowball method (paying off the smallest debt first for motivation) or the avalanche method (paying off the highest interest debt first for financial efficiency) can be effective strategies.

Strategies for Achieving Long-Term Goals

Achieving long-term financial goals requires a well-defined plan and a commitment to consistent action. This involves understanding different investment vehicles, managing risk effectively, and aligning your investment strategy with your specific objectives. A proactive approach to long-term financial planning can significantly improve your chances of achieving significant life milestones.Successful long-term financial planning hinges on selecting appropriate investment strategies and managing associated risks.

This section explores several key strategies and their implications.

Investment Strategies for Long-Term Goals

Long-term financial goals often benefit from a diversified investment portfolio. Stocks, bonds, and real estate represent three major asset classes, each with its own risk-return profile. Stocks, representing ownership in companies, generally offer higher potential returns but also carry higher risk compared to bonds. Bonds, which are essentially loans to governments or corporations, provide relatively stable income and lower risk.

Real estate investments, encompassing properties or land, can offer both income generation and potential appreciation, but often involve higher upfront capital and management responsibilities. The optimal mix of these asset classes depends on individual risk tolerance and time horizon. For example, a younger investor with a longer time horizon might allocate a larger portion of their portfolio to stocks, while an older investor closer to retirement might prefer a more conservative approach with a higher allocation to bonds.

Diversification and Risk Management in Long-Term Investment Planning

Diversification is crucial for mitigating risk in long-term investments. By spreading investments across different asset classes, sectors, and geographies, investors can reduce the impact of any single investment’s poor performance on their overall portfolio. Risk management involves identifying and assessing potential risks, developing strategies to mitigate those risks, and regularly monitoring the portfolio’s performance. This might involve setting stop-loss orders on individual investments or rebalancing the portfolio periodically to maintain the desired asset allocation.

For example, if the stock market experiences a significant downturn, a diversified portfolio might still retain value due to the presence of other asset classes like bonds or real estate. Conversely, a portfolio heavily concentrated in a single stock or sector is significantly more vulnerable to market fluctuations.

Long-Term Financial Planning and Significant Life Goals

Effective long-term financial planning plays a pivotal role in achieving significant life goals, such as retirement and homeownership. Retirement planning involves saving and investing sufficient funds to maintain a desired lifestyle after ceasing employment. This often requires regular contributions to retirement accounts, such as 401(k)s or IRAs, and careful consideration of investment strategies to maximize returns while minimizing risk.

Homeownership, another significant life goal, often requires substantial savings for a down payment and ongoing expenses like mortgage payments, property taxes, and insurance. A well-structured financial plan can help individuals save diligently for a down payment, secure a mortgage at favorable terms, and manage the financial obligations associated with homeownership. For instance, someone aiming for retirement at 65 might start contributing to a retirement account at age 25, allowing the power of compounding to significantly grow their savings over time.

Similarly, someone aiming for homeownership within five years might develop a strict savings plan, perhaps utilizing high-yield savings accounts and minimizing unnecessary expenses to accumulate the necessary down payment.

Balancing Short-Term and Long-Term Goals

Successfully navigating personal finances often involves juggling competing priorities. Short-term needs, like paying bills or covering unexpected expenses, demand immediate attention, while long-term aspirations, such as retirement savings or buying a home, require consistent planning and dedication. The key to financial well-being lies in effectively balancing these competing demands without sacrificing either short-term stability or long-term prosperity.Prioritizing short-term and long-term financial goals requires a strategic approach.

It’s not about choosing one over the other, but rather finding a way to integrate them seamlessly. This involves creating a comprehensive financial plan that considers both immediate needs and future ambitions. A well-defined budget, coupled with realistic saving and investment strategies, is crucial in this process.

Prioritization Strategies for Competing Financial Goals

Effective prioritization involves a careful assessment of your current financial situation and your future goals. Consider the urgency and importance of each goal. High-urgency, high-importance goals, such as emergency fund creation or debt repayment, should generally take precedence. Lower-urgency, high-importance goals, like retirement savings, should still receive consistent attention, even if contributions are smaller initially. A useful tool is to assign a numerical value (e.g., 1-10) to both the urgency and importance of each goal, then multiply these values to create a weighted score.

Goals with higher scores should be prioritized.

Potential Conflicts and Resolution Methods

Conflicts between short-term and long-term goals are common. For instance, the desire for a new car (short-term) might conflict with the need to aggressively pay down high-interest debt (long-term). Similarly, the temptation to spend a bonus on a vacation (short-term) might detract from contributions to a retirement account (long-term). Resolution often involves trade-offs and compromises. In the car example, delaying the purchase and prioritizing debt repayment could save significant interest and accelerate the path towards long-term financial security.

For the bonus example, allocating a portion to both the vacation and the retirement account can satisfy both immediate desires and long-term needs. The key is to find a balance that aligns with your overall financial plan.

Decision-Making Flowchart for Balancing Financial Priorities

The following flowchart Artikels a decision-making process for balancing competing short-term and long-term financial priorities.Imagine a flowchart with the following steps:

1. Start

Begin by listing all your short-term and long-term financial goals.

2. Assess Urgency and Importance

Assign a numerical score (1-10) for urgency and importance to each goal. Multiply the scores to get a weighted priority score.

3. Prioritize Goals

Arrange goals in descending order based on their weighted priority scores.

4. Allocate Resources

Allocate your available financial resources to the highest-priority goals first.

5. Regular Review and Adjustment

Regularly review your progress and adjust your plan as needed based on changes in your financial situation or priorities.

6. End

The process concludes with a balanced financial plan that accommodates both short-term and long-term needs.

The Role of Financial Planning and Auditing

Financial planning acts as the roadmap to achieving both short-term and long-term financial goals. It provides a structured approach to managing finances, ensuring resources are allocated effectively to meet various needs and aspirations. Without a plan, achieving financial goals becomes significantly more challenging, akin to navigating without a map. Regular financial auditing, on the other hand, offers a crucial mechanism for monitoring progress and making necessary course corrections.Effective financial planning involves a detailed assessment of current financial status, the identification of both short-term and long-term objectives, and the development of strategies to bridge the gap between the present and the desired future.

This includes budgeting, saving, investing, and debt management strategies tailored to individual circumstances. The process is iterative, requiring regular review and adjustments based on changing circumstances and emerging opportunities.

The Importance of Financial Planning in Achieving Financial Goals

Financial planning provides a clear framework for prioritizing goals. By outlining specific objectives with associated timelines and resource allocation, individuals can focus their efforts and make informed decisions about their spending and saving habits. For example, a young professional might prioritize paying off student loan debt (short-term) while simultaneously contributing to a retirement account (long-term). A well-defined plan allows them to balance these competing demands effectively.

Furthermore, financial planning facilitates informed decision-making regarding significant life events, such as buying a home, starting a family, or changing careers. By anticipating these events and planning accordingly, individuals can mitigate potential financial risks and seize opportunities. Without a plan, unexpected expenses can derail progress toward both short-term and long-term goals.

The Role of Regular Financial Auditing in Monitoring Progress

Regular financial auditing involves periodically reviewing one’s financial status against the established plan. This involves tracking income and expenses, monitoring investment performance, and assessing debt levels. This process allows individuals to identify areas where they are exceeding expectations and areas where they might be falling short. For example, if someone is consistently undersaving for retirement, the audit process can highlight this shortfall, prompting adjustments to the savings plan.

Similarly, if unexpected expenses arise, the audit can reveal the impact on the overall financial plan, enabling timely adjustments to spending habits or the exploration of alternative financing options. Without regular audits, individuals risk losing track of their progress, potentially jeopardizing the achievement of their goals.

Examples of Financial Advice Supporting Goal Achievement

Financial advisors provide invaluable support in setting and achieving financial goals. They can help individuals create a comprehensive financial plan tailored to their specific circumstances, considering factors such as income, expenses, risk tolerance, and time horizon. For instance, an advisor might recommend a specific investment portfolio aligned with an individual’s retirement goals, or suggest strategies for managing debt more effectively.

Advisors also provide ongoing support, offering guidance on adjusting the plan as circumstances change and providing objective feedback on progress. They can help individuals stay disciplined and focused on their long-term objectives, even when faced with unexpected challenges. Seeking professional financial advice can significantly enhance the likelihood of achieving financial goals, particularly for complex financial situations. For example, a couple planning for a large purchase like a house can benefit greatly from expert advice on mortgage options, budgeting for homeownership, and long-term investment strategies to build wealth.

Illustrative Examples

Understanding the interplay between short-term and long-term financial goals is best illustrated through real-world scenarios. This section provides examples showcasing how individuals can successfully manage both immediate needs and long-term aspirations.

Balancing Short-Term Savings with Long-Term Investments: A Young Professional’s Journey

Consider Anya, a 28-year-old marketing professional earning an annual salary of $75,000. She aims to save for a down payment on a condo within three years (short-term goal) while simultaneously investing for retirement (long-term goal). Anya’s strategy involves a multi-pronged approach. First, she allocates 20% of her post-tax income ($15,000 annually) towards her short-term goal. This is achieved through a high-yield savings account, contributing consistently every month.

This allows her to save approximately $1250 monthly. She projects needing a $60,000 down payment, making this savings plan sufficient. Simultaneously, she contributes 15% of her income ($11,250 annually) to a Roth IRA, aiming for tax-advantaged growth for retirement. This plan leverages the power of compounding, expecting substantial returns over the long term. She also contributes an additional 5% to her company’s 401(k) plan, taking advantage of any employer matching.

This combined approach allows Anya to diligently pursue both her immediate housing needs and long-term financial security.

Achieving Early Retirement Through Consistent Financial Planning and Auditing

Imagine David, a 40-year-old software engineer who dreams of retiring at 55. He meticulously planned his financial future, starting early with consistent investments and regular auditing of his portfolio. David’s strategy involved a diversified investment portfolio across stocks, bonds, and real estate. He started with a modest investment amount but consistently increased contributions as his income grew.

He regularly audited his investments, adjusting his portfolio allocation based on market conditions and his evolving financial goals. His annual financial audit involved reviewing his investment performance, analyzing his spending habits, and projecting his future income and expenses. This disciplined approach allowed him to identify areas for improvement and make necessary adjustments. Through consistent saving, strategic investing, and diligent auditing, David managed to accumulate a substantial nest egg by age 55, enabling him to retire comfortably ahead of schedule.

This demonstrates how a proactive and analytical approach to financial management can translate into the achievement of ambitious long-term goals.

Effective financial planning hinges on the ability to harmoniously balance short-term and long-term goals. By setting SMART objectives, implementing sound budgeting practices, and employing suitable investment strategies, individuals can create a financial roadmap that aligns with their aspirations. Regular monitoring and adjustments, informed by financial audits and professional advice, are crucial for staying on track and adapting to life’s changes.

Ultimately, achieving a secure and prosperous financial future involves a proactive and well-informed approach, blending immediate gratification with long-term vision.

Questions and Answers

What is the difference between an emergency fund and a short-term goal?

An emergency fund is a readily accessible pool of money for unexpected expenses (job loss, medical bills), while a short-term goal is a specific financial objective with a defined timeframe (e.g., saving for a vacation).

How can I adjust my goals if my income changes?

Regularly review and adjust your financial plan based on income fluctuations. You may need to prioritize certain goals or modify your savings/investment strategies accordingly.

What if I don’t meet a short-term goal?

Don’t be discouraged! Analyze why you fell short, adjust your budget or strategies, and refocus your efforts. Persistence is key.

When should I seek professional financial advice?

Consider seeking professional help when you have complex financial situations, need guidance on investment strategies, or require assistance with retirement planning.