Navigating the financial landscape as a small business owner can feel like charting uncharted waters. Success hinges on understanding not just your product or service, but also the intricate dance of income, expenses, and long-term financial planning. This guide provides a comprehensive overview of essential financial strategies, from securing funding to managing taxes and mitigating risks, empowering you to make informed decisions and steer your business towards prosperity.

We’ll explore key financial statements, budgeting techniques, funding options, and tax considerations, equipping you with the knowledge to build a robust financial foundation. We’ll also delve into crucial aspects like financial forecasting, risk management, and setting achievable financial goals. By understanding these elements, you can confidently navigate the complexities of small business finance and achieve sustainable growth.

Securing Funding and Financing

Securing sufficient funding is crucial for the success of any small business. The right financing strategy can fuel growth, overcome initial hurdles, and provide the necessary resources for expansion. Choosing the appropriate funding method depends heavily on factors such as the business’s stage of development, creditworthiness, and the nature of the business itself. Understanding the various options available and their associated implications is paramount.

Different funding options cater to various needs and risk profiles. Carefully weighing the pros and cons of each is essential before making a decision. Consider factors like interest rates, repayment terms, and the dilution of ownership when comparing these options.

Comparison of Funding Options for Small Businesses

Several avenues exist for securing funding, each with its own set of advantages and disadvantages. A thorough understanding of these options is vital for making informed financial decisions.

- Loans: Loans from banks or credit unions provide a relatively straightforward method of accessing capital. They require repayment with interest, but they don’t dilute ownership. However, securing a loan can be challenging for startups or businesses with poor credit history. Interest rates vary depending on creditworthiness and market conditions.

- Grants: Grants are essentially free money provided by government agencies or private foundations. They typically require fulfilling specific criteria and often support particular initiatives or industries. Competition for grants can be fierce, and the application process can be extensive. They don’t require repayment.

- Equity Financing: This involves exchanging a portion of the business ownership for capital. Venture capitalists or angel investors provide funding in exchange for equity stakes. This can provide significant capital injection but comes at the cost of relinquishing some control and future profits.

- Bootstrapping: Bootstrapping involves funding the business through personal savings, revenue generated, and cost-cutting measures. It avoids debt and equity dilution, but it can limit growth potential and require significant personal sacrifice.

Applying for a Small Business Loan: A Step-by-Step Guide

The application process for a small business loan can seem daunting, but a structured approach can increase the chances of approval. Thorough preparation is key to a successful application.

- Assess your needs: Determine the loan amount needed and the purpose of the loan. Develop a clear and concise business plan outlining how the funds will be used.

- Check your credit score: A good credit score significantly improves your chances of approval. Review your credit report and address any inaccuracies or negative marks.

- Gather necessary documents: Prepare all required documentation, including financial statements (profit and loss statements, balance sheets, cash flow statements), tax returns, business licenses, and personal financial information.

- Shop around for lenders: Compare loan terms, interest rates, and fees from different lenders (banks, credit unions, online lenders). Consider factors such as loan amount, repayment terms, and prepayment penalties.

- Complete the loan application: Fill out the application accurately and completely. Provide supporting documentation as requested.

- Negotiate terms: Once you receive a loan offer, review the terms carefully and negotiate if necessary. Ensure you understand all aspects of the loan agreement before signing.

Advantages and Disadvantages of Using Credit Cards for Business Expenses

Credit cards can offer convenience and flexibility for managing business expenses, but they also present potential risks if not managed carefully. Understanding both sides of the equation is crucial.

- Advantages: Credit cards provide a convenient method for tracking expenses, offer purchase protection, and can build business credit if used responsibly. They also often provide rewards programs, such as cashback or points.

- Disadvantages: High interest rates can quickly accumulate debt if balances aren’t paid promptly. Overspending is a significant risk, and late payments can negatively impact credit scores. Fees, such as annual fees and late payment fees, can add to the overall cost.

Tax Planning and Compliance

Navigating the tax landscape as a small business owner can feel overwhelming, but proactive planning is crucial for long-term financial health and success. Understanding your tax obligations and implementing effective strategies can significantly reduce your tax liability and minimize administrative burdens. This section Artikels key tax considerations and strategies for small business owners.Effective tax planning involves more than just filing your taxes annually.

It’s a year-round process that integrates seamlessly with your overall business financial strategy. Understanding the various taxes you’re responsible for and employing sound strategies for minimizing your tax burden are vital for maximizing your profitability.

Types of Taxes for Small Businesses

Small business owners typically face several types of taxes, the most common being income tax, sales tax, and payroll tax. The specific taxes applicable will depend on factors such as your business structure (sole proprietorship, partnership, LLC, S corp, C corp), location, and industry. Careful consideration of these tax obligations is essential for compliance and financial planning.

Income Tax

Income tax is levied on your business’s profits. For sole proprietorships and partnerships, business income and expenses are reported on your personal income tax return (Form 1040, Schedule C). Corporations (S corps and C corps) file separate corporate tax returns (Form 1120-S or Form 1120). Understanding deductions and credits available to businesses is crucial for minimizing your tax liability.

For example, the qualified business income (QBI) deduction can significantly reduce the taxable income for many small businesses.

Sales Tax

Sales tax is a consumption tax collected from customers on the sale of goods and services. Whether or not you need to collect sales tax depends on your state and local regulations. If you are required to collect sales tax, you must register with your state’s tax agency, remit the collected tax regularly, and keep accurate records of all sales and tax collected.

Failure to comply can result in penalties and interest.

Payroll Tax

If you employ others, you’ll be responsible for payroll taxes, including Social Security and Medicare taxes (FICA) and federal and state unemployment taxes (FUTA and SUTA). Payroll taxes are typically withheld from employee wages and matched by the employer. Accurate and timely payroll tax payments are crucial to avoid penalties. Understanding the intricacies of payroll tax withholding and reporting is critical.

Miscalculations can lead to significant financial repercussions.

Strategies for Minimizing Tax Liability

Minimizing your tax liability involves employing legal and ethical strategies to reduce your tax burden. These strategies should always be implemented in full compliance with applicable tax laws. Some common strategies include maximizing deductions, utilizing tax credits, and structuring your business appropriately.

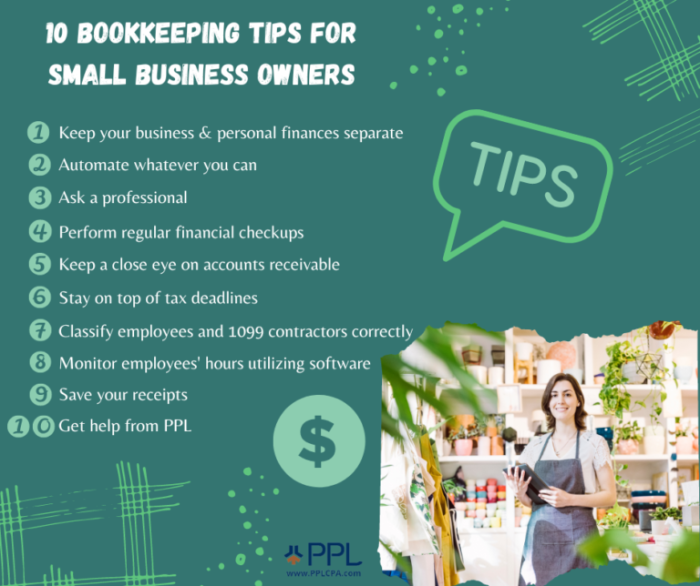

Importance of Accurate Record Keeping

Maintaining accurate and organized financial records is paramount for tax compliance. This includes keeping detailed records of all income, expenses, invoices, receipts, and bank statements. Accurate record-keeping simplifies tax preparation, minimizes the risk of errors, and facilitates efficient tax planning. It also helps in case of an audit by providing readily available documentation to support your tax filings.

Using accounting software can significantly streamline this process. For example, QuickBooks or Xero provide features for tracking income and expenses, generating reports, and managing payroll.

Financial Auditing and Risk Management

Maintaining a healthy financial standing requires more than just generating revenue; it demands a proactive approach to auditing and risk management. Regular financial audits provide valuable insights into your business’s performance, highlighting areas of strength and weakness, while effective risk management safeguards your company from potential financial setbacks. This section details the importance of both for small business owners.Regular financial audits are crucial for small businesses to maintain financial health and transparency.

They offer an independent verification of the accuracy and reliability of your financial records, providing confidence to stakeholders like investors, lenders, and even yourself.

The Financial Audit Process for Small Businesses

A financial audit for a small business typically involves a systematic examination of financial records, including income statements, balance sheets, and cash flow statements. The auditor, often a qualified accountant or CPA, will verify the accuracy of these records, ensuring compliance with accounting standards (like Generally Accepted Accounting Principles or GAAP). This process may include reviewing supporting documentation like invoices, receipts, and bank statements.

The auditor will then issue an audit report summarizing their findings, including an opinion on the fairness of the financial statements. The depth and scope of the audit will vary depending on the size and complexity of the business, and the requirements of stakeholders. For example, a business seeking a bank loan might require a more comprehensive audit than one that is solely owner-operated.

Common Financial Risks Faced by Small Businesses and Mitigation Strategies

Small businesses face a unique set of financial risks due to their size and limited resources. Understanding these risks and implementing effective mitigation strategies is paramount for long-term success.

- Cash Flow Problems: Insufficient cash flow is a leading cause of small business failure. Mitigation strategies include careful budgeting, efficient inventory management, and proactive invoice collection.

- Debt Management: High levels of debt can cripple a business. Strategies include responsible borrowing, negotiating favorable loan terms, and maintaining a healthy debt-to-equity ratio.

- Economic Downturns: External economic factors can significantly impact revenue. Mitigation involves diversification of revenue streams, building financial reserves, and developing contingency plans.

- Cybersecurity Threats: Data breaches and cyberattacks can lead to significant financial losses. Strategies include investing in robust cybersecurity measures, employee training, and data backup systems.

- Fraud: Internal or external fraud can severely damage a business’s finances. Mitigation strategies include implementing strong internal controls, regular audits, and background checks on employees.

The Role of Insurance in Protecting a Small Business from Financial Loss

Insurance plays a vital role in protecting small businesses from unforeseen financial losses. Various insurance policies can mitigate risks associated with property damage, liability claims, employee injuries, and business interruption.

- Property Insurance: Protects against damage or loss to business property, including buildings, equipment, and inventory.

- Liability Insurance: Covers legal costs and damages resulting from claims of negligence or wrongdoing.

- Workers’ Compensation Insurance: Protects against costs associated with employee injuries or illnesses sustained on the job.

- Business Interruption Insurance: Covers lost income and expenses resulting from unforeseen events that disrupt business operations.

Choosing the right insurance coverage is crucial. Consult with an insurance professional to determine the appropriate level of protection for your specific business needs and risk profile. The cost of insurance is a significant expense, but the potential financial consequences of being uninsured often far outweigh the premiums.

Building a thriving small business requires more than just a great product or service; it demands a solid understanding of financial management. This guide has provided a framework for navigating the key financial aspects of running a successful small business. By implementing the strategies and advice Artikeld here, you can enhance your financial literacy, minimize risks, and ultimately achieve your business objectives.

Remember, proactive financial planning is an investment in your business’s future, leading to greater stability, profitability, and long-term success.

FAQ Insights

What are the common signs of financial trouble for a small business?

Consistent cash flow problems, inability to meet payroll, increasing debt, declining sales, and difficulty securing loans are all warning signs.

How often should I review my financial statements?

Ideally, review your income statement, balance sheet, and cash flow statement monthly to track performance and identify potential issues promptly.

What is the difference between equity financing and debt financing?

Equity financing involves selling a portion of your business ownership in exchange for funds, while debt financing involves borrowing money that needs to be repaid with interest.

How can I improve my business credit score?

Pay bills on time, maintain a low debt-to-credit ratio, and monitor your credit reports regularly for errors.